The Metabolic Transformation

Endocrinology and metabolic disease therapeutics have undergone a once-in-a-generation commercial and scientific revolution. The GLP-1 receptor agonist class -- originally a niche diabetes franchise -- has become the most commercially consequential drug category of the decade, reshaping investor expectations, payer policy, prescriber behavior, and competitive strategy across not just endocrinology but cardiology, nephrology, hepatology, and neurology simultaneously.

For small and micro-cap biotech and pharma companies operating in the metabolic space, the GLP-1 era presents a dual challenge: the anchor mechanisms are dominated by large-cap incumbents (Novo Nordisk, Eli Lilly) commanding extraordinary market positions, while simultaneously opening entirely new therapeutic sub-segments -- rare metabolic disorders, combination approaches, novel mechanisms addressing the failures of GLP-1 monotherapy -- where emerging companies can compete on differentiation rather than scale.

This Deep Insight report provides the market intelligence, pipeline analysis, commercial framework, and strategic imperatives necessary to navigate the metabolic therapeutics landscape with precision in 2025.

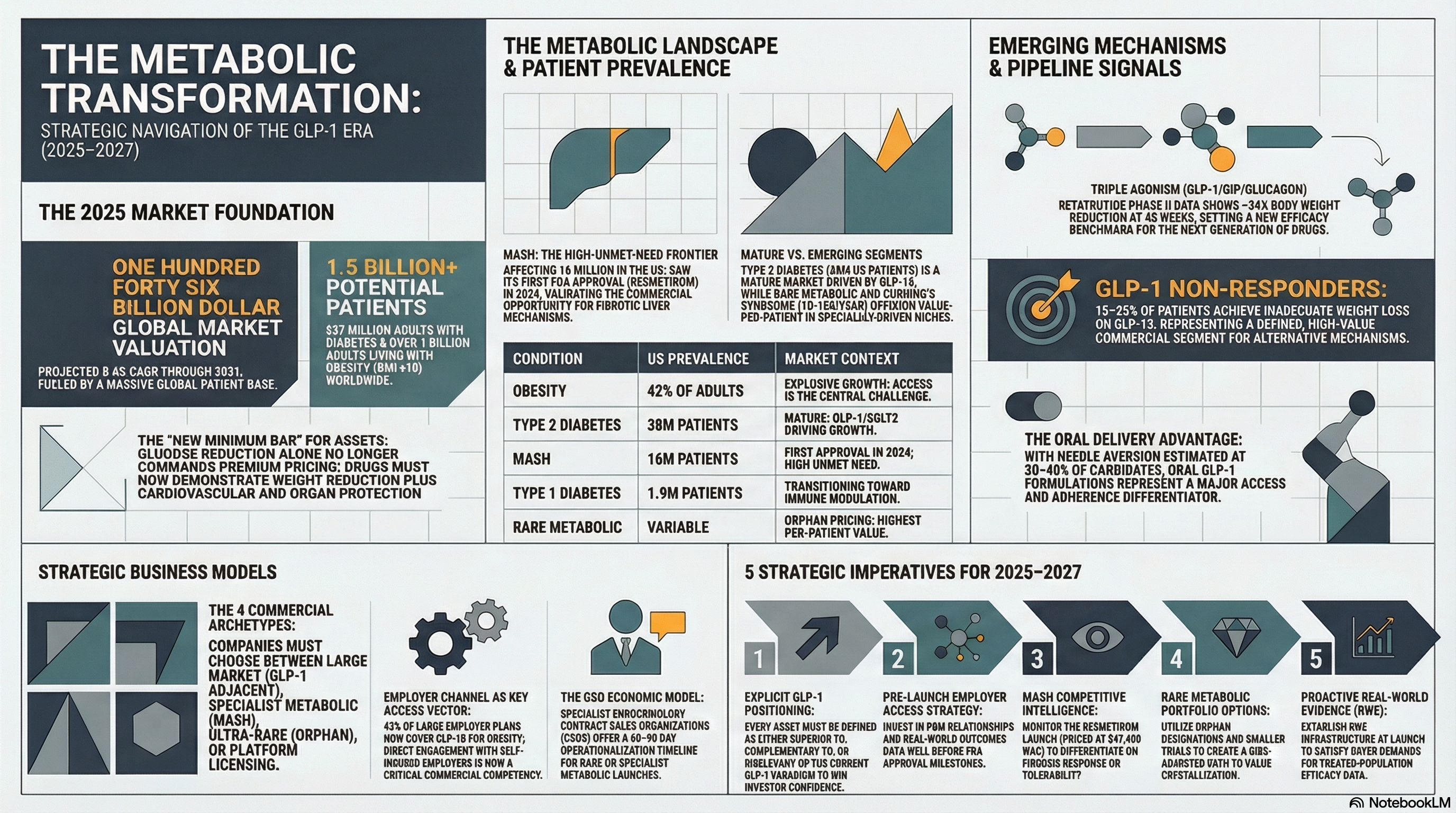

$146B

Global metabolic therapeutics market (2024)

8.4%

Projected CAGR through 2031

537M

Adults with diabetes worldwide

1B+

Adults with obesity globally (BMI >=30)

Strategic Signal: GLP-1 Has Changed the Rules -- For Everyone

Semaglutide and tirzepatide have reset what investors, payers, and clinicians expect from any metabolic drug. Glucose reduction alone no longer commands premium pricing or formulary priority. The new minimum bar is weight reduction plus cardiovascular protection plus an emerging organ-protection story. Emerging companies must position their assets relative to this reality -- either as complementary to GLP-1 therapy, superior in defined populations where GLP-1 fails, or in metabolic indications where GLP-1 is irrelevant.

Market Landscape & Epidemiological Foundation

1.1 The Metabolic Disease Spectrum

The endocrinology and metabolic therapeutic category encompasses conditions with vastly different epidemiological profiles, commercial dynamics, prescriber bases, and payer environments. Understanding the distinctions is foundational to commercial strategy:

| Condition | US Prevalence | Commercial Landscape Notes |

|---|---|---|

| Type 2 Diabetes | 38M patients | Mature market; GLP-1/SGLT2 driving growth; generics dominant in older classes |

| Obesity (BMI >=30) | 42% of US adults | Explosive growth; access still constrained; employer benefit expansion accelerating |

| Type 1 Diabetes | 1.9M patients | Insulin-dependent; teplizumab (immune modulation) first disease-modifier approval |

| Non-Alcoholic Steatohepatitis (MASH) | 16M with MASH in US | First approvals in 2024 (resmetirom); high unmet need; GLP-1 activity expanding |

| Hypothyroidism / Hyperthyroidism | 20M+ patients (hypo) | Largely genericized; niche opportunity in Graves disease / thyroid eye disease |

| Cushing's Syndrome | ~10-15K diagnosed/yr | Rare; specialist-driven; high value per patient; pipeline active |

| Acromegaly / GH Disorders | ~25K US patients | Ultra-rare; established specialist network; multiple pipeline agents |

| Rare Metabolic / Lysosomal Storage | Variable by condition | Orphan pricing; gene therapy entrants; highest per-patient value in portfolio |

1.2 The GLP-1 Disruption Effect on Market Architecture

The market impact of GLP-1 receptor agonists extends far beyond their direct commercial performance. They have structurally altered the competitive environment across the entire metabolic landscape:

Payer Access as the Central Challenge

Obesity pharmacotherapy faces a unique access paradox: clinically proven efficacy in reducing cardiovascular events (SELECT trial, semaglutide 2.4mg: 20% MACE reduction), yet commercial insurance coverage for obesity treatment remains inconsistent. Only 43% of large employer health plans cover GLP-1 drugs for obesity as of 2024. For emerging companies in the obesity space, payer strategy is not a post-approval consideration -- it is the central challenge of the business model.

The Next Frontier: GLP-1 Combination Therapy

As GLP-1 monotherapy becomes standard of care, the pipeline has moved to combination approaches: GLP-1/GIP dual agonists (tirzepatide), GLP-1/glucagon dual agonists, GLP-1/amylin combinations, and oral formulations for patients intolerant of injectable therapy. Each combination creates new competitive positioning opportunities for emerging companies -- particularly those with differentiated delivery mechanisms or novel receptor targets.

GLP-1 Non-Responders as a Commercial Opportunity

Approximately 15-25% of patients on GLP-1 therapy achieve inadequate weight loss (<5% body weight reduction). This population -- now identifiable with reasonable precision -- represents a defined commercial segment for complementary or alternative mechanisms. Emerging companies developing agents that work in GLP-1 non-responders have a clearly bounded, high-value patient population story to tell investors and payers.

Continue reading the full report

Enter your details below to unlock all 30+ pages of this Deep Insight report instantly.