The Cardiovascular Imperative

Cardiovascular disease (CVD) remains the leading cause of death globally, accounting for 17.9 million lives annually -- nearly one-third of all global mortality. Yet the commercial and strategic landscape for cardiovascular therapeutics is undergoing its most profound transformation in a generation. The convergence of novel mechanism classes, precision medicine infrastructure, and a dramatic reshaping of payer dynamics has created both exceptional opportunity and elevated strategic complexity for small and micro-cap biotech and pharma organizations navigating this space.

This Deep Insight report synthesizes the most critical market intelligence, pipeline signals, commercial frameworks, and strategic imperatives relevant to cardiovascular therapeutics executives in 2025. It is designed to serve as a working strategic reference -- not a literature review -- and is structured to inform decisions across commercial launch planning, business development, partnership strategy, and investor narrative construction.

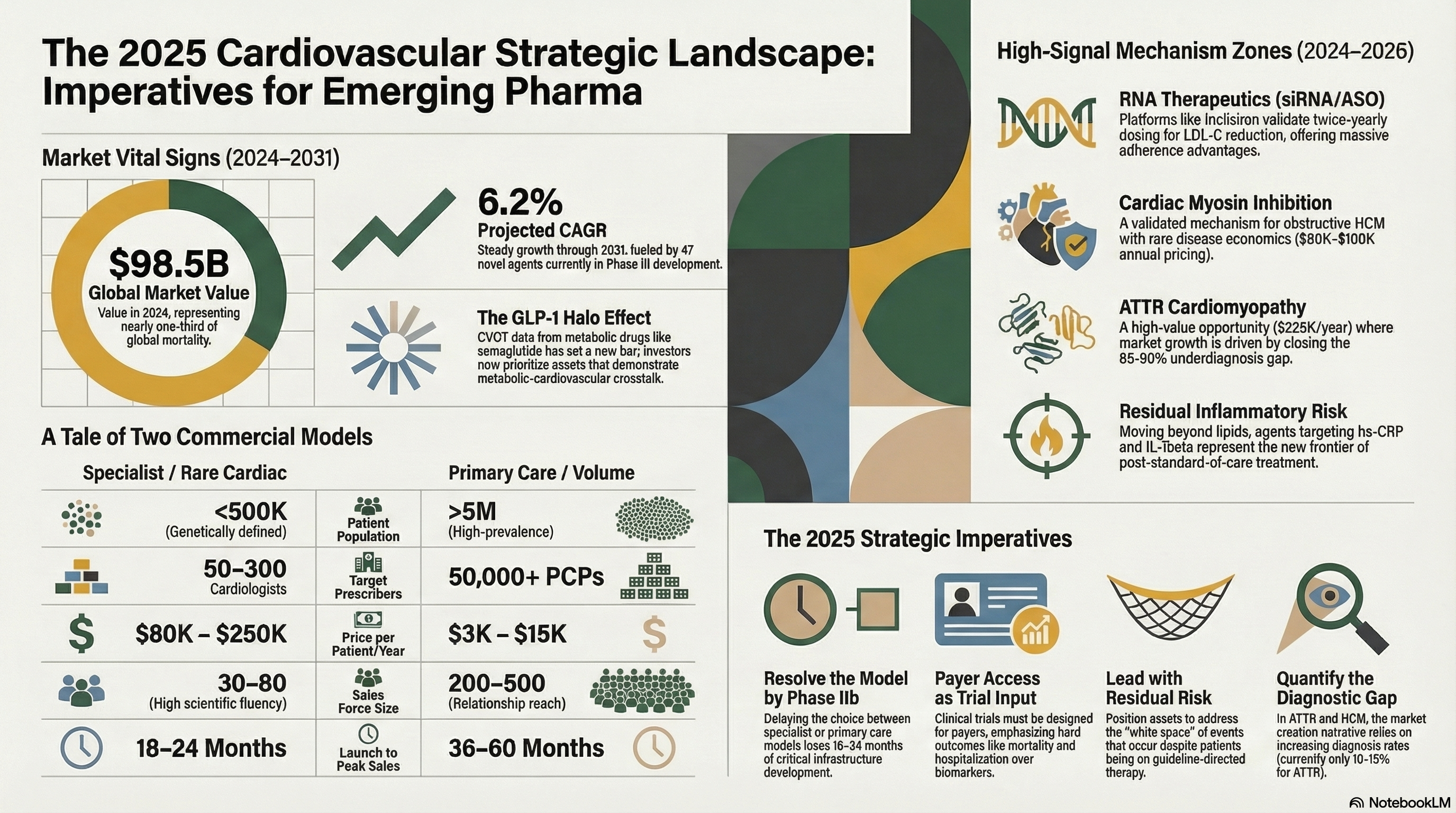

$98.5B

Global CVD therapeutics market (2024)

6.2%

Projected CAGR through 2031

523M

People living with CVD globally

47

Novel CVD agents in Phase III (2025)

Strategic Signal: The GLP-1 Effect Is Reshaping the Entire Cardiovascular Pipeline

The CVOT data from semaglutide and tirzepatide have fundamentally altered investor and payer expectations for what a cardiovascular drug must demonstrate. Pure lipid-lowering or anti-hypertensive mechanisms face significant headwinds unless linked to hard endpoint differentiation. For emerging companies, this raises the bar -- and the opportunity -- for agents that can credibly claim metabolic-cardiovascular crosstalk as part of their mechanism story.

Market Landscape & Epidemiological Foundation

1.1 The Burden of Disease

Cardiovascular disease encompasses a heterogeneous family of conditions -- ischemic heart disease, heart failure, atrial fibrillation, peripheral artery disease, hypertension, and cardiomyopathies among the most commercially significant. Understanding the relative epidemiological weight of each subtype is the first discipline of commercial strategy, because payer access, prescriber behavior, and patient journey architecture differ dramatically across them.

| CVD Subtype | US Prevalence & Key Commercial Notes |

|---|---|

| Heart Failure (HFrEF / HFpEF) | 6.7M patients; bifurcated market -- HFpEF remains the largest underserved segment |

| Atrial Fibrillation | 6M+ patients; anticoagulation dominant; rhythm control pipeline accelerating |

| Ischemic Heart Disease | 18M patients; generics dominant; residual risk is the commercial white space |

| Hypertension | 116M patients; enormous generic penetration; differentiation requires hard endpoint data |

| Hypertrophic Cardiomyopathy (HCM) | ~700K patients; rare/ultra-rare economics; high value per patient |

| ATTR Cardiomyopathy | ~400K diagnosed; massively underdiagnosed; fastest-growth rare cardiac sector |

| Dyslipidemia (elevated Lp(a)/LDL-C) | 93M+ patients; PCSK9i penetration <5% eligible; adherence and access gap |

| Peripheral Artery Disease | 8.5M patients; few novel agents; meaningful unmet need in revascularization |

1.2 Structural Market Dynamics

Several macro forces are reshaping the competitive environment in ways that disproportionately affect emerging companies relative to large-cap incumbents:

The Generics Cliff Is Both Threat and Opportunity

Major cardiovascular franchises -- including ACE inhibitors, ARBs, and beta-blockers -- are deeply genericized, suppressing pricing in primary prevention. This creates white space for novel mechanisms addressing residual risk in treated patients. The commercially sophisticated emerging company frames its asset not as a replacement but as a complement -- targeting the gap that guideline-directed therapy leaves behind.

Payer Sophistication Has Permanently Increased

Post-Inflation Reduction Act, payer scrutiny of cardiovascular drug pricing has intensified significantly. Step therapy requirements, prior authorization burdens, and outcomes-based contracting are now standard operating environment. Emerging companies that engage payer strategy at Phase II rather than Phase III will achieve a structural advantage in time-to-formulary access.

The Cardiology-Metabolic Boundary Has Dissolved

GLP-1 receptor agonists generated landmark CVOT data (LEADER, SUSTAIN-6, SELECT) establishing cardiovascular mortality benefits independent of glycemic control. This has permanently blurred the boundary between endocrinology and cardiology, with major implications for prescriber targeting, competitive framing, and BD pipeline valuation for companies in the metabolic-cardiovascular overlap.

Continue reading the full report

Enter your details below to unlock all 30+ pages of this Deep Insight report instantly.