The Immunology Inflection Point

Immunology and inflammation therapeutics has emerged as the single most commercially productive category in all of pharmaceuticals over the past two decades -- and the innovation cycle shows no sign of slowing. From the original TNF inhibitor revolution through JAK inhibitors, IL-targeting biologics, and now cell therapy and precision immune modulation, the immune-mediated disease space has consistently generated blockbuster revenues, premium pricing, and durable competitive moats for companies that establish early leadership in defined patient populations.

For small and micro-cap biotech and pharma companies, the immunology landscape in 2025 presents a dual reality: it is among the most competitive categories in terms of mechanism crowding -- particularly in the IL-17, IL-23, JAK, and anti-TNF spaces -- yet simultaneously offers extraordinary white space in rare autoimmune conditions, precision-defined patient subsets, and next-generation mechanisms that address the fundamental limitations of current standard of care.

This Deep Insight report provides the strategic intelligence framework for immunology and inflammation executives navigating this complex, high-value landscape in 2025.

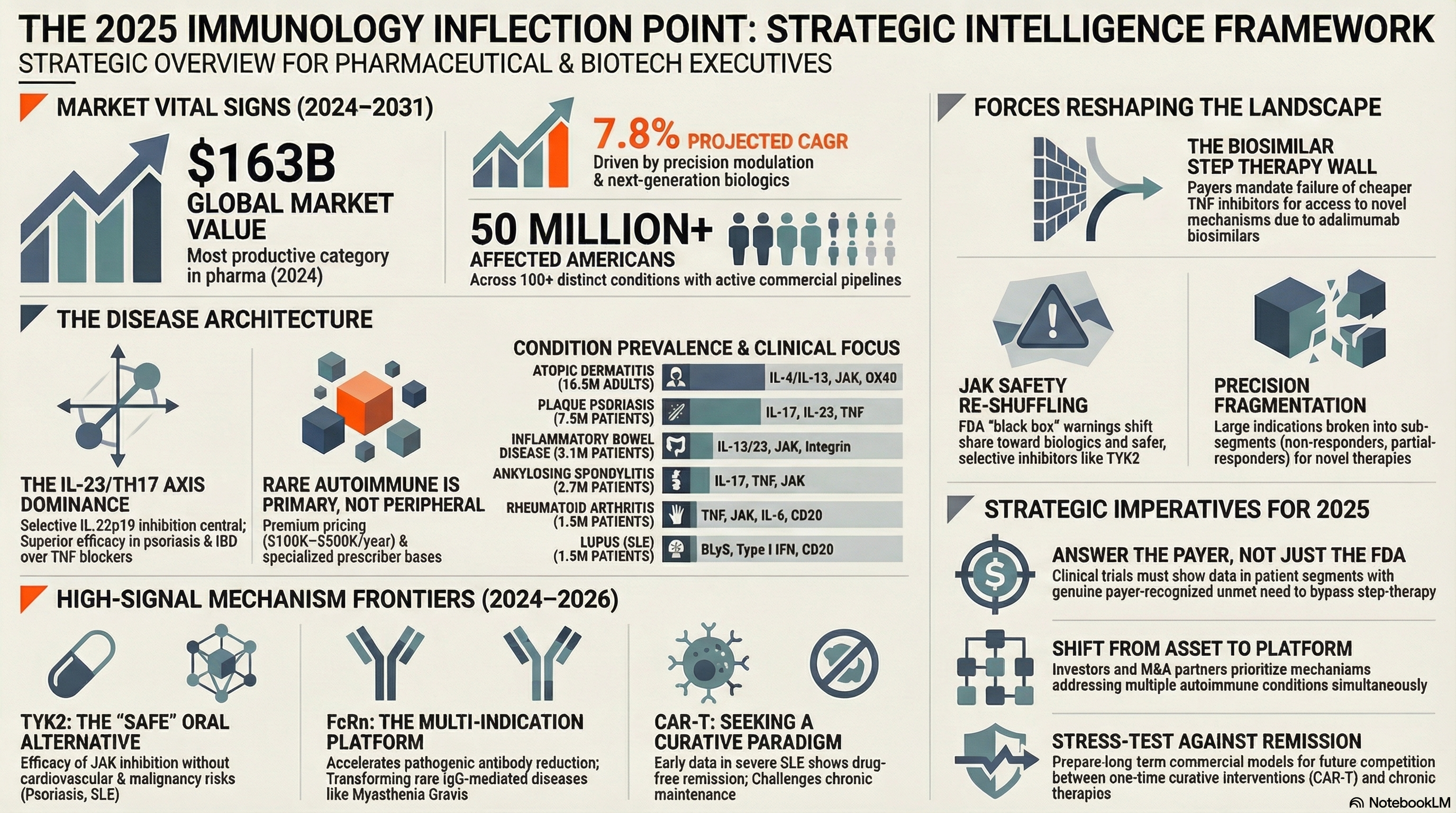

$163B

Global immunology therapeutics market (2024)

7.8%

Projected CAGR through 2031

50M+

Americans with autoimmune disease (AARDA)

100+

Distinct autoimmune conditions with commercial pipeline activity

Strategic Signal: The IL-23/TH17 Axis Has Become the Central Immunology Battleground

Selective IL-23p19 inhibition (risankizumab, guselkumab, tildrakizumab) has demonstrated superior efficacy and durability versus IL-17 inhibitors and TNF blockers across psoriasis, PsA, and IBD -- reshaping the treatment algorithm across multiple indications simultaneously. For emerging companies, this creates both a competitive crowding challenge in established indications and a template for mechanism-led expansion: any company that can demonstrate a new indication for IL-23 pathway modulation is working from a validated commercial playbook.

Market Landscape & Disease Architecture

1.1 The Immune-Mediated Disease Spectrum

The immunology and inflammation category spans conditions with vastly different epidemiological profiles, specialist ownership, payer dynamics, and commercial models. The strategic distinctions matter enormously for commercial planning:

| Condition / Segment | US Prevalence | Dominant Mechanisms | Commercial Notes |

|---|---|---|---|

| Plaque Psoriasis | 7.5M patients | IL-17, IL-23, TNF | Mature but innovating; high switching; biosimilar pressure on older agents |

| Rheumatoid Arthritis | 1.5M patients | TNF, JAK, IL-6, CD20 | Biosimilar erosion of originator TNFis; JAK safety label changes shifting mix |

| Psoriatic Arthritis | 1M patients | IL-17, IL-23, JAK, TNF | Combination skin + joint efficacy the differentiator; high-value specialist segment |

| Inflammatory Bowel Disease | 3.1M patients (UC + CD) | IL-12/23, TNF, integrin, JAK, IL-23 | Fastest-growing autoimmune segment; TNF-naive and TNF-experienced require different positioning |

| Atopic Dermatitis | 16.5M adults | IL-4/IL-13 (dupilumab), IL-31, JAK | Dupilumab dominance; OX40, IL-33 pipeline active; primary care + derm crossover |

| Ankylosing Spondylitis / AxSpA | 2.7M patients | IL-17, TNF, JAK | Early non-radiographic axSpA emerging as distinct commercial segment |

| Lupus (SLE) | 1.5M patients | BLyS, Type I IFN, CD20, complement | Historically difficult; anifrolumab/belimumab establishing new standard |

| Myasthenia Gravis | ~70K patients | FcRn, complement, CD20 | Rare; premium pricing; FcRn inhibitors transforming the treatment landscape |

| Rare Autoimmune Conditions | Variable (<100K each) | Complement, FcRn, IL-targeted | Orphan economics; premium per-patient; specialist-concentrated prescribing |

1.2 Three Structural Forces Reshaping the Landscape

Biosimilar Pressure Is Restructuring the TNF Inhibitor Foundation

Adalimumab (Humira) -- the world's best-selling drug at peak -- lost US exclusivity in 2023, triggering the largest biosimilar wave in immunology history. Over 10 adalimumab biosimilars have entered the US market, with WAC pricing 40-85% below originator. This has structurally shifted payer step therapy algorithms, forcing all branded immunology agents to demonstrate meaningful clinical differentiation from biosimilar adalimumab -- not just from the originator. For emerging companies, this raises the clinical bar while simultaneously accelerating patient movement to novel mechanisms.

JAK Inhibitor Safety Label Revisions Have Reshuffled the Market

The FDA's 2021 black box warning additions to all JAK inhibitors -- covering MACE, malignancy, thrombosis, and mortality risk -- fundamentally altered prescribing patterns, particularly in older patients and those with cardiovascular risk factors. This has created commercial opportunity for biologics with cleaner safety profiles in those populations, and has elevated the safety differentiation story for next-generation selective JAK inhibitors (TYK2, JAK1-selective, JAK3-selective) now in late-stage development.

Precision Immunology Is Fragmenting Large Indications Into Addressable Sub-Segments

Type 2 inflammatory disease (atopic dermatitis, eosinophilic esophagitis, chronic rhinosinusitis with nasal polyps, prurigo nodularis) has been validated as a precision-definable patient population by dupilumab's multi-indication approvals. The same logic is now being applied across TH1, TH17, and mixed inflammatory endotypes. For emerging companies, this creates an opportunity to define commercially valuable patient sub-segments within large indications where existing therapies achieve only partial response -- the non-responder, the partial-responder, and the safety-limited patient are now definable and targetable populations.

Continue reading the full report

Enter your details below to unlock all 30+ pages of this Deep Insight report instantly.